The Initial Phase – Financial Crisis Unfortunately, the depth and length of the crisis are currently being discounted. At the moment, the crisis is in its initial phases. What is taking place only has affected mostly the financial sector; there has been only a minimal effect on the real economy. However, at the latest by next year, the second phase of the crisis will begin, with spillover effects into the economy. In 2009, the weakness of the global economy will become central. The current economic system is built on providing loans in ever increasing amounts, not on saving and the repayment of debt over time. If a private person builds his life on a series of new loans, where he repays old debt with new debt, then he would be considered crazy and would inevitably end up either in debtor's prison or bankruptcy. If the same thing were to take place at the corporate and state level, then nobody would dare say anything. It would be considered perfectly normal. Where is the child from the fairytale who wasn’t afraid to cry out that the king was naked! Companies have become accustomed to taking new loans, although the financial system is attempting to correct. A contraction of bank credit to the private sector is in place, and inevitably the economy will not receive the money (read: credit) that it was planning on receiving. In addition, financial companies are unable to sell financial securities to finance themselves, since even the currently successful companies that kept free funds in shares and securities in order to earn a higher return, have lost over half of their value. This first initial phase is well familiar to us. We have lived with it for almost two years. The media has called it by various names: “The Subprime Crisis”, “The Credit Crunch”, and “The Credit Crisis”. The

Second Phase – Economic Crisis The lack of money becomes evident in the second phase of the crisis – the financial crisis is replaced by an economic crisis, triggering massive bankruptcies that would spread globally in a chain reaction. After the series of initial difficulties encountered by home borrowers and the construction companies, there have been no bankruptcies so far in manufacturing, shipping, media, food processing, not to mention luxury goods like luxury cars, yachts and watches, or exotic businesses like space tourism. But their time will come. During the second phase of the crisis, another large sum of capital will “evaporate” from the market, because a company which is going bankrupt will leave nothing for shareholders and very little for its bondholders. In the second stage of the crisis, unemployment will begin to grow along with the wave of bankruptcies. The final quarter of 2008 is only the beginning. Remember that in 1931-1932, the unemployment rate in the USA was 20%, with one in five people unemployed.

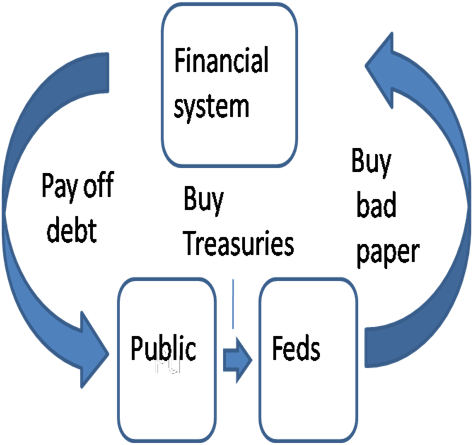

The Third Phase – Hyperinflation Throughout the series of crises, politicians will attempt to interfere in the game, but the third stage of the crisis will nevertheless begin. Since banks were “saved” with large bailouts, politicians will also begin to lavish corporations with various aid packages. The recent charade of automakers begging for money is only the beginning. Thus, measures will be undertaken that, in the opinion of politicians, will help the economy and save jobs, something that will likely become known as Obama’s “New New Deal”. This will include a multitude of spending programs and, above all, the loaning of credit with astronomical increases in the money supply, together with the classifying of the corresponding numbers into the trillions. Just like now nobody talks any more in terms of millions, so in the not so distant future no one will be talking any more in terms of billions. Trillions will be the order of the day. Perhaps bank lending standards will be relaxed. Perhaps the government will lavish the banks with a lot more money than it does today, just to keep them lending. Perhaps the central bank will directly monetize private debt. Perhaps the government will guarantee many more corporate loans, just like it recently guaranteed the securities/loans of the GSEs. Perhaps GSEs will proliferate throughout the economy, transforming the U.S economy into the “GSE Economy”, transforming a former great capitalist economy into a modern-day nationalsozialistische economy. Perhaps the government will implement all of the above. It will seem for awhile that peace has arrived, that the crisis has been overcome, as if the bankrupt companies have been “saved”, although this will only be the calm before the storm. If there is already more money in the financial system than actual goods, then after the subsequent injections of money, more like dropping money from helicopters or showering corporations with money, the economic ship will begin to heel. In this stage, the third stage, the hyperinflation scenario will begin when people realize that the money in banks will buy them next month half as much as it did this month. Then panic will ensue. People will begin to buy essential and non-essential items, just as long as there is something of value that can be obtained in exchange for their colourful pieces of worthless paper. Manufacturing enterprises would no longer want to sell goods, because the money received in exchange for the sale of their goods is not sufficient to purchase the new raw materials. Everyone who sells an actual object or good for paper money is a loser, since the same money is no longer enough to purchase again the same goods. Money created out of thin air electronically has brought tremendous benefits to the initial users and issuers, but at the expense of the wider masses through the collapse in their standards of living in this stage. The third phase will be chaotic and difficult. The details are difficult to predict, but if history is any judge, the politicians won’t be asleep. They will likely pass a number of important laws, prices will be fixed, wages will be standardized, foreign currency accounts will be frozen; in general, everything that could be done, will be done, and this will only serve to extend the agony. Social upheaval and riots will be suppressed by brute force; many democratic freedoms and values will likely be lost. As of today, the hyperinflation spiral and Zimbabwe Syndrome have reached the point of no return.

Final Phase – Monetary Collapse In the event that democracy survives, then the fourth and final phase will begin, a phase which can be called The Darkness before Dawn, the final agony before the rising of the sun. This is the ultimate destruction of the monetary and financial system, the loss of all electronic and financial values that is accompanied by monetary reform throughout most of the world. In the worst case scenario, this will result in the creation of a Global Government; in the best case scenario, the process will take place separately in each country. For example, at the end of the Tulip Mania of the 17th century, all futures transactions with which tulips were bought and sold for millions of florins were declared void. Similarly, all electronic assets, contracts, securities, and futures contracts will be declared void, because the world doesn’t have a court or executive power which is capable of enforcing bankruptcies and debt collection resulting from millions of non-performing contracts. Only the actual collateral for loans will be demanded - land, houses, apartments. The losers will be private persons, while legal entities, along with their debts and non-existent collateral, will be lost in the virtual world, the place from whence they came. Things will begin again with a clean slate. We will once again all be on an equal level. Railroads and planes, bridges and houses won’t disappear. All real wealth will remain, lost is only the paper wealth, those things that people believed they had and that they believed someone else (read: government, banks, pension funds, etc) will preserve for them. At that moment, faith will truly have been lost, as the fruits of a person’s life will have, through several metamorphoses, been transformed into banking sector profits and executive bonuses that had been spent by the suits long before the crisis even began. The new economic system will be different than the current one. Its type, shape, or form is impossible to predict at the moment. Similarly to the end of the slave-holding system, it was not possible to see the creation of the feudal system. It was also impossible to foresee the blossoming of capitalism before the industrial revolution in England in 1785. So, it now is impossible to predict all the changes, although those changes are inevitable. Each process must go through its historical development and must reach its natural conclusion. History shows that every changeover from one organisation of society to another has been very painful. Nevertheless, each following step, no matter how painful, has moved humanity forward and offered a better life to more people. Hopefully it will also go forward this time. All we have to do is hang on.

“How Not to Invest” Paperback May 5!

2 hours ago